“You should talk to these guys.”

— Serving Clients Nationwide Since 1979 —

(also called accounts receivable or A/R financing)

Once your customer is approved and your invoice is verified,

we usually send your money within

24 hours.

Before you decide, we show you the numbers in writing — what you get now (“advance”), what’s set aside until your customer pays (“reserve,”), and the cost (“fee”).

Either way, you need your money sooner than the

30, 45, 60, or even 75-day terms you gave your clients.

Either way you need your money before the

30, 60, or 75-day terms you gave your customers.

A lot of the time, the wait isn’t the work. It’s the paperwork.

PO match, receiving, and missing backup are what hold invoices up.

Whether you're in CNC machining, pallet manufacturing, plastics manufacturing, food processing, or packaging, the story is the same. You ship the order. The invoice is out. But your bills are due first.

Machine shops. Metal fab. Plastics. Packaging. Food.

Different work. Same wait to get paid.

So what do you do while you’re waiting?

Your customer wants Net-30, Net-60, or Net-75. To win the job, you agree. No matter the terms, your bills still show up on time.

Materials, payroll, rent, electricity bill, insurance…

The bills keep coming while you wait out those terms. You can put some costs on a card, but the statement comes due before your customer pays.

Wait too long and you’re the one

stuck with late fees or interest.

Okay. So what’s the fix?

We're Orange Commercial Credit. We buy invoices for work you’ve already done. This is called invoice factoring.

We’ve been doing it since 1979 — for over 45 years! Different economies. Same problem: customers on terms, bills due now.

Here's how one client put it:

“Within a day the money is in my account.”

—Val, Owner and Client Since 2017

In manufacturing, it usually looks like this: you shipped the order, the invoice is out, and your customer is on Net-30, Net-60, or Net-75.

Here's how it works with us:

Once you're set up as a client, you send us the invoice and the backup your customer requires (PO + shipping/receiving proof). We review it and if it’s approved, we send most of the money up front.

That up-front payment is called an advance. Depending on your industry, it can be as high as 90% or higher of the invoice.

When your customer pays in full, on the next cycle you receive the remainder minus our fee, which can range from 1.25% - 5%.

After approval, funds are often sent within 24 hours. Timing depends on the invoice and the setup. You pick which invoices to sell.

Use it when you need it, skip it when you don’t.

You know how it is: materials, payroll, rent, electric bill, insurance. Those bills don’t wait.

Over the years we’ve worked with manufacturers just like you. Many have been with us for over five years.

They stay because the money’s there when they need it and because they value the service they receive.

“We have the capital we need the very day we send invoices in… She understands our client and works with us to process invoices quickly.”

—Jill, Synergy Solutions

They have one dedicated account executive who is backed by an experienced team ready to answer all their questions.

Most of our business comes from referrals. Our clients refer because they know their friends will get the same service they do.

Those referrals come from all over manufacturing. Here’s the kind of work we fund every day — shipped orders with invoices out, while the customer pays on terms:

With us, even if your customer pays on 30, 60, or 75-day terms, you’ll have the cash in your account, usually within 24 hours of invoice approval once you’re established as a client.

One customer. One invoice. One call.

You get a person, not a menu.

1-800-231-3878

The only way this works is if your customer’s good for it. That’s why our credit check matters.

We’ve been doing this since 1979, and many of our credit team members have been here 10+ years. They know how to check credit right.

We focus on getting you paid faster on approved invoices.

It’s one thing to hear you’ll get paid...

Here’s what happens, step by step, from the time you send an invoice until the final payment clears.

In invoice factoring, the first thing we do is check your customer’s credit. We pull their payment history up front—even before you send us an invoice—because that’s how we decide if we can buy the invoice from you.

A client since 2013 put it this way:

“Credit checks come back same day… and we get funded when we need it.”

—E.H., President, Pallet Manufacturer (Atlanta, GA)

Once your customer is approved, you send an invoice, and our team then reviews the supporting paperwork that goes with it.

Most of the time it’s not complicated. It’s one missing detail: PO number, line items that don’t match, or missing shipping/receiving proof.

One thing to know in manufacturing: the terms don’t always start on the invoice date. They often start when your customer accepts the invoice in their system.

And even after it’s accepted, many customers still pay on a schedule. If a chargeback or dispute happens, you handle it with your customer directly. Once the payment is received, we release the reserve and send the remaining funds to you, as per the terms.

Once your invoice is approved and you're set up as a client, we notify your customer to send payment directly to us and confirm they’ve accepted the change.

It doesn’t change the work you did or the price on the invoice. It updates their Accounts Payable on where to send the payment.

The last step is the funding, the part you care about most.

That’s when the money is deposited in your account.

On every funding you’ll see:

For some manufacturing industries, we can advance up to 90% or more of an approved invoice within 24 hours. On a $10,000 invoice, that usually means $9,000 or more up front.

Once you're set up, the steps are the same across all your locations. Whether you're based in one city or have multiple plants across regions, we handle each invoice the same way, so you have a more predictable way to plan week to week.

If you bill out of an ERP or a customer portal, that’s fine. SAP, Oracle, or something else — we work with what you already use. What we need is the invoice and the backup your customer requires.

Once the invoice is approved and your customer has updated remittance to Orange Commercial Credit, we send the funds.

When a reserve applies, we set aside a small portion until your customer pays. It helps protect you against having to pay us out of pocket for any uncollectible portions of your invoices.

We release the available reserve balance, minus our discount fee, once a month.

The discount fee depends on:

Before you decide, we show you the numbers in writing: what you get now (the advance); what’s set aside until your customer pays (the reserve); and the fee.

Once you're set up and after the initial funding, our factoring looks like this:

Ready to see your numbers? Call and we’ll walk you through one invoice on the phone:

1-800-231-3878

The difference with us? We’re independent, so we can set terms that fit your business.

We don’t answer to outside investors. We’re privately held.

Your terms come from us — and no one else.

We’re business owners too. We know what it takes to meet payroll and keep the lights on.

And we also know every manufacturing company runs a little differently. We don’t drop numbers into a formula. We look at your invoices and your customers.

We base terms on what we see in your invoices and your customers, not on a one-size-fits-all chart.

And a client for several years put it this way:

“OCC was recommended by our bank, they worked with us to get a line established even though we didn’t fit into a regular business profile. We have multiple emergency water hauling contracts and OCC took these into account. Also their system is well automated and prompt, runs like clockwork!”

—Joel, Water Services for Municipalities

In the end, it comes down to trust. Who do you want to rely on when bills don’t wait?

Start simple: one customer, one invoice, one call.

You’re probably asking: So how would this work in my shop?

It depends on the work you do and how your customers pay.

For manufacturing, the pattern is usually the same: you ship product, you send the invoice, and your customer pays on terms. For CNC shops, it’s about meeting tight deadlines while dealing with high-value parts. For pallet manufacturers, it’s about managing fluctuating lumber prices and core collections. For plastics, it’s handling tooling costs and mold invoices.

The pain isn’t just “Net-60.” The pain is when the invoice is rejected, payment is delayed, or they only pay on a set schedule. With factoring, we review your PODs, Pack Slips, and CofCs the moment you upload them. The goal is to catch errors on Day 1, not Day 30.

So let’s talk manufacturing.

If you run a shop, whether it's a CNC operation, a job shop, or a Tier-1 supplier, you know the order of events. You pay first. Your customer pays later — often on Net-Terms or with a Just-in-Time (JIT) model.

And here’s what holds it up: they don’t pay until the invoice is accepted in their system.

If something is missing, the invoice gets rejected and you have to resend it. And payment is delayed.

Most of the time it’s simple stuff. They want the paperwork to match — things like your PODs, Pack Slips, and CofCs.

By the time you ship and gather all of that, you’ve already cut checks weeks ago. And you’re still waiting on their payment day.

And this is where factoring helps in manufacturing.

You send the invoice with the backup. We review your PODs, Pack Slips, and CofCs the moment you upload them. If we see something missing, we tell you early—so you can fix it before there’s a delay.

Once we can verify it, we send you the money — usually within 24 hours once you’re set up. Your customer pays us. Then the reserve is released.

Now, let’s talk about how this works for different types of manufacturers. Each one’s a bit different, and understanding what they need can make the process a lot easier for you.

Lumber gets paid before the order ships. Nails and fuel get paid too. Heat-treating costs come due too. Payroll doesn’t wait.

The work happens fast: cut boards, build to GMA specs (48x40), stack, and load.

And if you’re building ISPM-15 heat-treated pallets or crates for export (invoice factoring for pallet manufacturers), you’re paying those costs before your customer’s pay date.

And if you do recycled pallets, core collections and credits can make billing messy. Same with lumber surcharges when prices move.

Then you deliver. The invoice goes out. And the customer pays on Net terms.

What usually delays payment is matching the PO number, pallet count, and receiving details. If one piece is missing, the invoice gets rejected.

If your customer runs JIT delivery and wants unitized loads, they still won’t release payment until receiving is closed out.

So if the invoice gets rejected, you have to resend it, and then you’re waiting again.

With factoring, we look at the invoice and backup first and point out what we notice up front. We can't catch everything, but we can help reduce avoidable delays.

What we usually need with pallet & packaging invoices:

A pallet manufacturer told us how OCC became part of their growth:

“I’ve been working with OCC for over 9 years now and they’re like a partner for me.

I could not have grown my business this quickly without them!

My account executive is great.

I get credit checks done same day on new business and have never had a complaint from any customer.”

—E.H., President, Pallet Manufacturer (Atlanta, GA)

You bought the bar stock. You ran the CNC. The order shipped.

Cut it, machine it, deburr it, inspect it, box it up. In a job shop, the work can be done — and you’re still waiting on Net-60 or Net-75.

And if you’re working under AS9100 or ISO 9001, the paperwork has to be as tight as the tolerances.

Machine shop invoices get held up when details don’t match: PO number, line items, part numbers, rev levels, quantities, dates.

The other hold-up is backup. If the CofC, material certs, heat-treat certs, or inspection reports are missing, the invoice gets rejected — and payment is delayed.

What we usually need with machine shop invoices:

If the invoice gets rejected, you resend it — then you’re waiting again. With factoring, we review the invoice and backup up front and point out what we notice, so you can fix it right away and reduce delays.

A manufacturing owner told us what it felt like after switching to OCC:

“I used OCC several years ago and they were very good...now using them again and they are excellent! My account rep is extremely efficient, knowledgeable and communicates very well. So glad they are still around after all these years!

”

—Sharon, Manufacturing company

Resin gets bought before you ship. The power to run the presses gets used before you ship. Payroll needs to be paid, no matter when the customer pays.

In injection molding and plastic extrusion, the costs start the moment the first cycle starts. Cycle times, press tonnage, scrap — it all adds up while you’re still waiting on the pay date.

Run the press, trim parts, pack them, stage the shipment. Then the invoice goes out.

And it’s not just one process. Injection molding, extrusion, blow molding, thermoforming — it’s the same story.

Sometimes there’s tooling & molds too. A shop may bill the mold before production begins. That’s a milestone invoice, and the paperwork still has to match.

Even when the PO and part numbers match perfectly, many Tier-1 and Tier-2 buyers still follow their own internal payment schedules. They don’t pay on your terms—sometimes, they only process payments on specific dates, like the 1st and 15th of the month. So even if your invoice is perfect, you might end up waiting longer than expected for payment.

One of the most common delays in plastics billing is a resin surcharge that doesn’t match the customer’s index. We help verify the price adjustment against the PO so the invoice matches before we fund it.

And if you’re holding inventory or safety stock for a customer, you’re paying for material and space while you wait for payment.

What we usually need with plastics invoices:

Here’s how it works with factoring: invoice + PO + shipping/receiving proof. We review the invoice and backup and point out what we notice. If it’s approved, we send the funds.

Packaging costs add up quickly. Utilities come due in no time. Payroll needs to be paid on time.

Whether you’re a co-packer for a national brand or a private label manufacturer for a regional grocery chain, you pay for the run before you get paid for the run.

Run the line, pack the product, label it, ship it. Then you’re waiting on Net terms.

And the invoice still has to clear their system. In food, that often means the required backup is attached — including FSMA logs and lot tracking when the customer expects it.

Another real one: retailers can hit you with chargebacks, slotting fees, or spoilage allowances. That’s part of why food invoices can get short-paid.

If your customer requires receiving or a sign-off, that’s part of what we look for before we approve the invoice.

Many customers don’t start counting from the invoice date. They start when the invoice is accepted in their system.

Whether you’re doing PCB assembly, sub-assemblies, or full box builds, the costs hit before the pay date.

Pick parts, do the kitting, build it, test it, pack it, ship it. Don’t let your cash get tied up in WIP (work in progress) while you wait on Net terms.

And the invoice still has to clear their system: PO number, part numbers, quantities, and line items.

If a customer is looking for a reason to reject it, missing backup is the easiest one. CofC and testing logs are what stop the “rejection” or RMA delay.

If something doesn’t match, the invoice gets rejected. Then payment is delayed until the next cycle.

Factoring keeps you paying your bills on time, while your customers pay on their schedule.

If you run a pallet shop, machine shop, plastics shop, or packaging line, you’ve heard it:

“Can you give us Net-30?”

Sometimes Net-45. Buyers ask for it every day. And if you can’t offer it, they move on. With factoring in place, you can say yes without tying up your own cash.

Longer terms can:

“Factoring has been instrumental in helping us grow and expand our business without any cash flow disruptions.”

—Jorge, President and Owner, Client Since 2009

What matters most is whether your customer pays, and whether the invoice matches their PO and receiving.

In manufacturing, most delays come from the same place: PO match, receiving, and missing backup.

Things like tax liens or pledged invoices can slow things down, but we'll talk it through with you.

If we can help, we'll say so fast. If not, we'll tell you that too. No guesswork.

Call us and we'll go over one of your customer's invoices together.

Often it starts when your customer accepts the invoice in their system. That can be after receiving.

If the invoice gets rejected back and resent, you’ll have to wait again.

Missing PO number, line items that don’t match the PO, missing packing list, missing shipping/receiving proof, or missing receiving/QC sign-off when the customer requires it.

Put the PO number on it. Match the line items to the PO. Include part numbers, quantities, and ship date.

Attach what your customer requires: packing list, shipping proof, and receiving or QC sign-off if they ask for it.

The goal is this: the invoice matches the PO and receiving the first time.

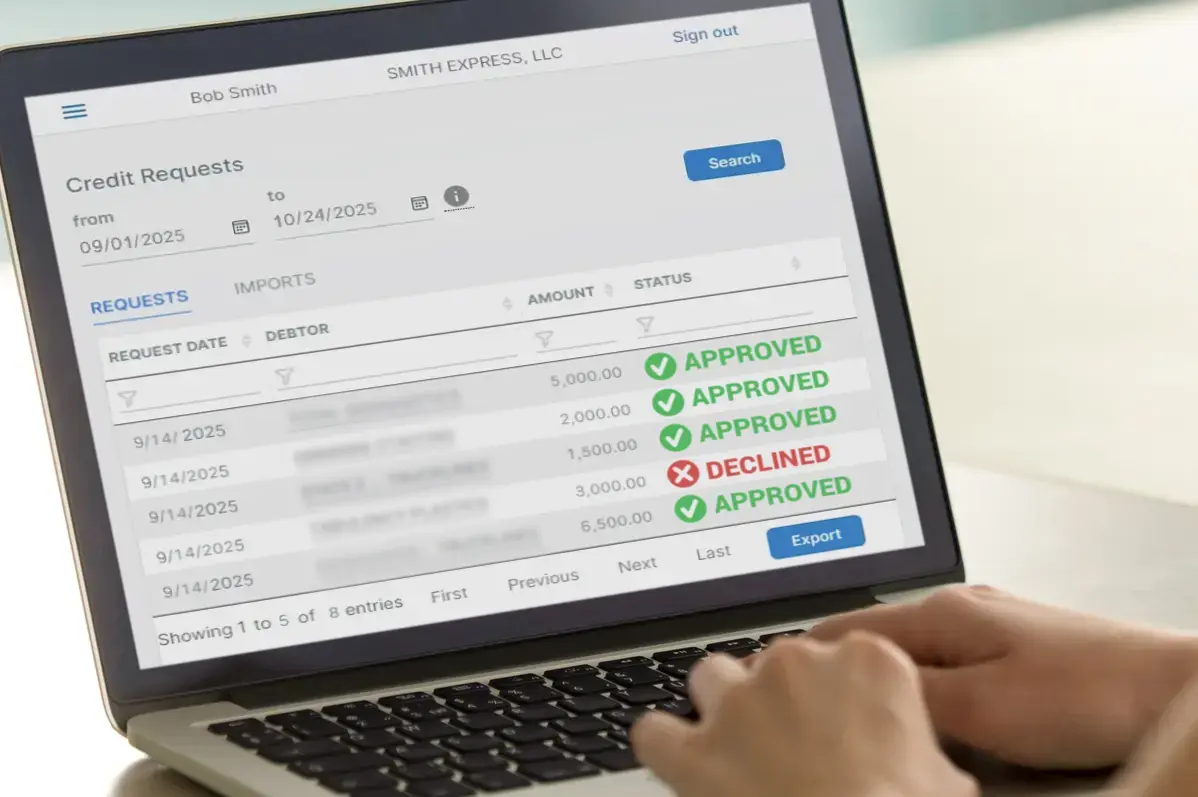

At Orange Commercial Credit, our portal shows every invoice and payment — status, paperwork, and credit — so you can see where you stand.

You don’t have to wonder

if a payment was posted right.

You can see if it’s waiting on something — like a missing PO number or missing shipping/receiving proof — instead of finding out weeks later.

Your paperwork is handled by our team who’ve been here on average 10 years and know your paperwork and your customers.

Yes. If your customer pays on a set pay run, factoring can still fund you after approval so you’re not waiting for the next cycle.

At Orange Commercial Credit, you get a dedicated account executive. They know you, your business, and your paperwork.

You talk to the same person who knows your account.

A contract manufacturer told us what it’s like working with OCC:

“My account rep and her team are very easy to work with and responsive. They’ve worked with me to solve problems/issues. I get explanations instead of being sent a document that I have to go through. Very happy with the relationship.”

—Mac, Precision Contract Manufacturing

No. Invoice factoring isn’t a loan. You sell an invoice for product you already shipped. There’s no new debt.

It depends on the customer, but most manufacturing invoices come down to a few items: the PO, the invoice, and shipping/receiving proof.

If your customer requires it, we may also need a packing list and a receiving or QC sign-off. The goal is this: PO number, line items, and shipping/receiving proof match the first time.

It depends on how your customer accepts and pays. If they pay per shipment, we can look at each invoice tied to that shipment.

If they require final delivery before they pay, we’ll tell you up front.

Short-pays happen in manufacturing. If a customer holds part of an invoice, we look at what they paid and why.

When the invoice is paid in full, the reserve releases (if a reserve applies).

If your customer disputes part of the invoice, you’ll handle the dispute with them directly. Factoring helps by ensuring that your invoice and all related paperwork — like the PO, shipping proof, and other required documents — are in order before we advance the funds. This reduces the chance of disputes happening in the first place.

Sometimes, yes. It depends on the customer and their payment history. Call and we’ll look at one customer and one invoice with you.

A little. Not the work — the paperwork.

The basics stay the same: your invoice must match the PO and receiving documentation (and QC sign-off, if required). This is where portals come in — they act as the gatekeeper.

If one field is off in the portal, the invoice can sit in “pending” or be rejected, causing delays.

These are just a few examples of the portals commonly used in manufacturing:

The discount fee is a percentage of the invoice. It depends on your customer’s credit, how fast they pay, and the invoices you sell.

You always see the cost up front before you decide.

No. You choose which invoices to sell. Most clients start with just one — like a $5,000 shipped-order invoice.

If you sell to other businesses, ship product, and bill on terms, it usually fits.

The main question is whether your customer pays, and whether the invoice has the PO number and shipping/receiving proof. Call us and we’ll look at one customer and one invoice with you.

No. They keep the same price and terms from you.

As the last step in the funding process, we contact your customer to verify the invoice and set up the payment change of address.

If your customer has a question or something’s missing, you work it out with them directly. Once it’s fixed, we move the funding forward.

Most of our team’s been here ten years or more. They spot issues early, so you’re not waiting long once everything’s approved.

If the product is still on your shop floor and hasn't shipped yet, it usually won't fit.

Call and we’ll tell you fast if an invoice works or not.

Yes. Receivables factoring, accounts receivable factoring, A/R funding, and A/R financing are all ways people describe the same thing: selling your unpaid invoices for shipped orders so you don’t wait on Net terms.

“Finding out about OCC has helped keep my business operating with the cash flow I am now receiving. Within a day the money is in my account. During the whole process, OCC was very easy to work with. They made sure I was completely confident and work with me step by step, and the staff is very patient. I would recommend them to any business. Once you start with OCC, you will also be recommending them.”

—Val, Owner and Client Since 2017, Machine Shop

But it’s not on you.

We get it.

There’s no setup fee and no obligation,

and most times you’ll have an answer

by the next business day.

If the proposal looks right to you, we'll set up an agreement. We work off a 90-day factoring agreement, but you're never required to submit any certain number of invoices. It's there when you need it.

The agreement lays out the basics:

For subsequent fundings after a new client is set up and their first invoice is approved, the advance is usually sent within 24 hours.

The chain looks like this: invoice → approval → money sent to your bank → your customer pays us → reserve released.

An auto repair and parts re-fabricator put it this way:

“Orange Commercial Credit has allowed my companies to grow yearly. With their cash flow we went from one business to a total of nine different businesses over the course of 10 years. I highly recommend it if you want to take your business to the next level. If I could give 10 stars I would.”

——Veronica, Nashville, TN – various companies and industries

No minimums, no quotas. You decide when to use it.

You also get a dedicated account executive who knows your business and picks up when you call — answering your questions on the spot.

And you can log in any time day or night to check on balances and invoices.

If it makes sense, great. If not, you’ll still leave knowing more than you did before.

And for the owners who don't put it off,

here’s what it looks like:

On subsequent fundings to repeat customers, the money’s in your account typically within 24 hours.

Payroll runs. Materials get bought. The power bill gets paid.

That’s why we tell owners:

if the numbers make sense, don’t wait.

Most owners start with just one invoice — enough to see how the numbers work.

In the end it always comes

back to the same thing:

one customer,

one invoice,

one call.

“The OCC team are very responsive and easy to work with.

We've been a customer for 15+ years and value our relationship.”

—Peggy, Electronics

For a real conversation:

1-800-231-3878

🌙

After hours? No problem.

After hours, or if you’d rather not call, fill out this form and we’ll call you back.