“You should talk to these guys.”

Serving Clients Nationwide Since 1979

Invoice factoring for Tacoma, Pierce County, South Sound, and Washington businesses that bill B2B customers on terms.

(also called accounts receivable financing or A/R financing for Tacoma businesses)

Orange Commercial Credit is an independent, privately held factoring company headquartered in Olympia, Washington, that works directly with Tacoma and Washington businesses that invoice B2B customers on terms.

We buy approved unpaid invoices for trucking, staffing, manufacturing, and other B2B companies so you can get paid before your customer’s 30, 60, or 75-day terms end.

Once your customer is approved and your invoice is verified,

we usually send most of the money within

24 hours.

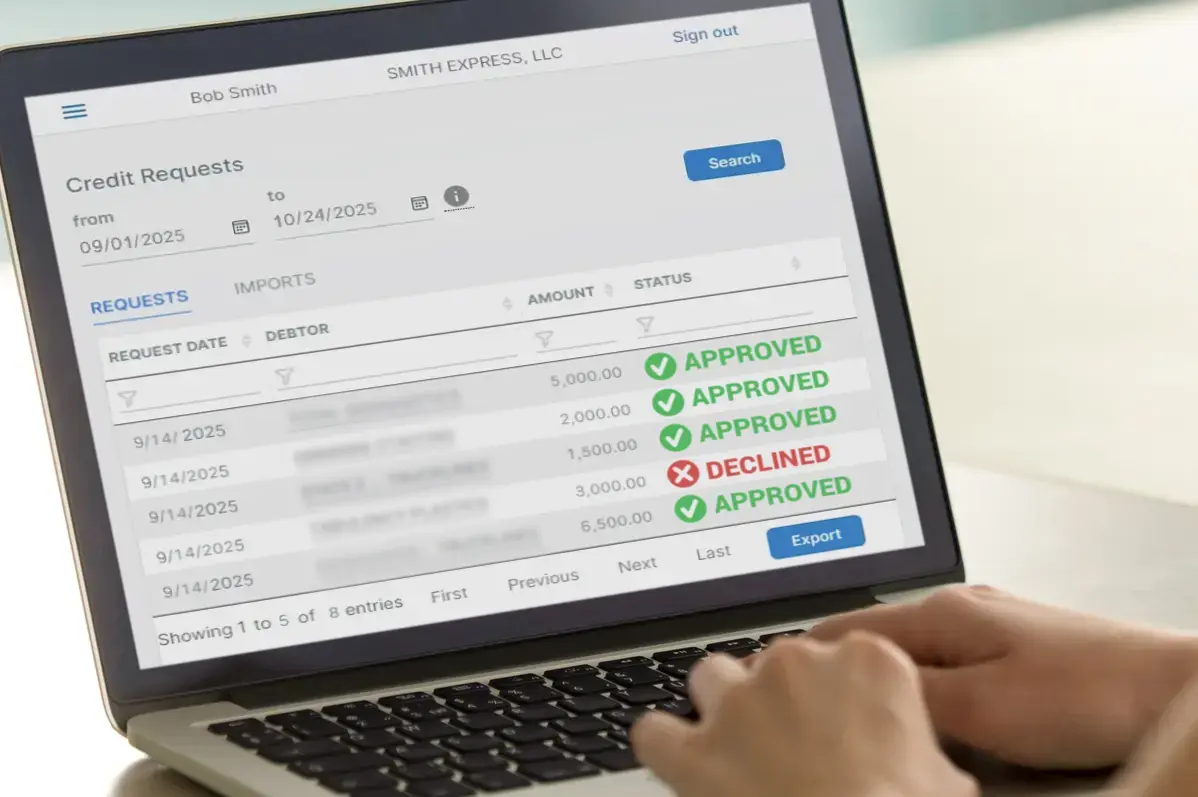

Before you decide, we show the numbers in writing: the advance, any reserve, the fee, payment instructions, and funding timing.

A factoring company buys approved unpaid B2B invoices so a business can get paid before its customer pays on terms. If you are comparing Tacoma factoring companies or invoice factoring companies, start with one real customer and one real invoice.

The written quote should show the advance, any reserve, fee, paperwork needed, payment instructions, funding timing, agreement terms, invoice choice, and who answers after setup.

A Tacoma factoring search may show local Tacoma firms, an Olympia headquarters listing, Seattle-Tacoma regional providers, local brokers, very-early-stage business programs, Washington directories, national ranking lists, and national factoring companies serving Tacoma and Pierce County.

Search can also show a directory profile whose company name includes Tacoma even when the listed business is based in another state, plus cold-storage, logistics, financial-consulting, or loan listings that do not buy approved unpaid invoices.

Orange Commercial Credit is a national independent direct factoring company serving Tacoma, Pierce County, South Sound, Washington, and Pacific Northwest businesses with a 90-day factoring agreement, no setup fee, no minimum number of invoices, invoice choice, written terms, and account support after setup.

Orange Commercial Credit is headquartered in Olympia, Washington. A factoring company does not need a Tacoma office to factor approved invoices for a Tacoma business.

That is because approval is based on commercial credit review, payment-history information, invoice verification, and the backup paperwork tied to the completed work. It is not based on the factoring company’s address.

The map tells you who appears close. The quote tells you more: who reviews the customer, checks the invoice, shows the written numbers, and answers after setup.

You do not need everything ready before the first call. One customer and one invoice are enough to see what the advance, fee, reserve, and timing could look like.

For Tacoma, Pierce County, South Sound, Washington, and Pacific Northwest businesses, we show the customer review, invoice review, advance, any reserve, fee, funding timing, agreement terms, invoice choice, and account support before you decide.

You may have heard about us from a friend, or you may be comparing Tacoma factoring companies after a search. However you got here, the pressure is usually the same.

You need the money before your customer pays on

30, 60, or 75-day terms.

The work’s already done. The invoices are out. And your bills are piling up, unpaid, while you’re left waiting.

Trucking. Staffing. Manufacturing.

Different work. Same wait.

Your customer wants 30, 45, or even 60-day terms. To win the business, you agree. No matter the terms, you still have bills to pay.

Payroll, fuel, insurance,

materials, equipment, repairs...

The bills keep coming while you wait out those terms. You can put expenses on a card while you wait, but the card bill comes due long before your customer pays.

Wait too long and you’re the one

stuck with late fees or interest.

If you are comparing factoring companies or invoice factoring companies, start with the items that affect your cash this week: advance rate, fee, reserve, customer approval, paperwork review, customer notice, funding timing, agreement terms, invoice choice, and who answers after setup.

Start with one real customer and one real invoice. The written quote should show what happens before funding, where the customer sends payment, and when any reserve can release.

A Tacoma search can show local-office signals such as a Tacoma address, an Olympia headquarters listing, a Seattle-Tacoma regional page, a local phone number, a map listing, reviews, or ratings.

It can also show a very-early-stage business program, a low-monthly-revenue program, a local broker, a Washington directory, a national ranking list, or a company profile whose name includes Tacoma even when the company is based elsewhere.

Claims may include rates from 0.69% to 1.59%, advance rates from 75% to 95%, a startup fee, a one-year contract, ACH or wire fees, no-fee broker wording, same-day funding, 24- to 72-hour funding, 2- to 5-day funding, or 3- to 5-day setup. Ask which conditions and fees apply to your real customer and invoice.

Use the search list to collect names. Then compare what the quote shows: the advance, any reserve, fee, paperwork needed, payment instructions, funding timing, agreement terms, invoice choice, and who answers after setup.

If a Tacoma result advertises a business loan, line of credit, equipment finance, purchase-order funding, asset-based lending, receivables administration, or another finance product, compare that separately from invoice factoring for completed B2B work.

For trucking and freight factoring companies, also compare broker credit checks, rate confirmation review, bill of lading or POD review, fuel-card terms, fuel-bundle terms, carrier-service terms, app and load-board terms, 24/7 funding claims, recourse or non-recourse wording, monthly minimums, invoice choice, and switching terms.

For staffing factoring companies and payroll funding providers, also compare approved-timesheet review, customer approval, weekly payroll timing, reserve release, monthly minimums, invoice choice, back-office service terms, payroll-processing terms, and switching terms.

For manufacturing invoice factoring, compare purchase-order review, packing-list or delivery-proof requirements, signed QC paperwork when required, supplier timing, reserve terms, and who answers when the paperwork does not match the invoice.

The written numbers are what let you compare the quote without guessing.

Orange Commercial Credit is a national independent direct factoring company headquartered in Olympia, Washington, and serving Tacoma, Pierce County, South Sound, and Washington businesses without requiring a Tacoma office visit.

A Tacoma business can start by phone or email with one customer, one invoice, and the backup paperwork tied to the completed work.

The table below is for the search results you may be sorting through: Tacoma office details, Olympia map listings, Seattle-Tacoma regional pages, local brokers, early-stage business programs, directory profiles, provider names that include Tacoma, fast-funding claims, fuel-card offers, staffing or payroll-funding claims, software or receivables-administration claims, bank-backed offers, and loan-company claims.

After you have the names, compare the written terms behind each one: who reviews the customer, who checks the invoice, what advance is offered, whether a reserve applies, what fee applies, and who answers after setup.

| What you see in search | What to check before you choose |

|---|---|

| Tacoma office, Olympia headquarters listing, Seattle-Tacoma regional page, local phone number, map listing, reviews, or ratings | Who reviews the customer, invoice, and paperwork, who sends the advance, and who answers after setup. |

| Very-early-stage or low-monthly-revenue program | Whether the offer is invoice factoring, what minimum or maximum volume applies, which customers qualify, and what setup, monthly, or transaction fees apply. |

| Low rate, 75% to 95% advance, startup fee, one-year contract, ACH fee, or wire fee | Whether the full fee schedule, reserve, minimums, agreement length, renewal, exit terms, and transfer-fee triggers are shown in writing. |

| Same-day, 24- to 72-hour, 2- to 5-day, or 3- to 5-day wording | Whether the claim refers to application review, setup, customer approval, invoice verification, or the actual advance, and which cutoff and bank-timing conditions apply. |

| Freight specialization, free credit check, fuel card, fuel bundle, app, load board, or carrier-service offer | Whether the broker or shipper can be approved, the load paperwork supports the invoice, and the extra service changes fees, minimums, invoice choice, agreement terms, switching terms, or account support. |

| Payroll funding, staffing factoring, or back-office offer | Whether the company buys approved unpaid staffing invoices or offers payroll processing, tax filing, timekeeping, recruiting, or another service with different costs and responsibilities. |

| Software, receivables administration, credit management, or payment-tracking offer | Whether the provider buys approved invoices or only manages billing, collections, reporting, or software. |

| No-fee broker, marketplace, directory, consultation, or referral listing | Who actually funds the invoice, whose agreement you sign, who services the account, and how the broker or marketplace is paid. |

| Business loan, credit line, equipment finance, purchase-order funding, asset-based lending, or working-capital offer | Whether the offer is invoice factoring or debt with different collateral, repayment, reporting, and exit terms. |

| A company name that includes Tacoma even though the profile lists another state | The company’s actual location, who funds the invoice, and whether the listed terms apply to your Tacoma business. |

| Customer notice or collection wording | What your customer sees, where your customer sends payment, who answers payment questions, and who works through a dispute or short pay. |

| Cold-storage, logistics, financial-consulting, or other business-service listing | Whether the listing actually buys approved unpaid B2B invoices, verifies the invoice, sends the advance, and services the account after setup. |

A factoring company does not need a Tacoma office to factor approved invoices for a Tacoma business.

That is because customer approval is based on commercial credit review, payment-history information, invoice verification, and the backup paperwork tied to the completed work. It is not based on the factoring company’s address.

Before you decide, the written quote should show the advance, any reserve, fee, payment instructions, funding timing, agreement terms, invoice choice, and who answers after setup.

If the written terms work for you and you choose to set up the account, you can email the invoice and backup paperwork or upload the invoice packet through the client portal. After setup, you work with a dedicated account executive backed by an experienced team.

Once your customer is approved, the invoice is verified, and the account is set up, we send the advance. Your customer sends payment according to the written instructions. When payment posts to our bank, any available reserve releases under the agreement terms.

One customer and one invoice are enough to see whether the numbers work.

When you search Tacoma factoring companies, the first results may be Tacoma office listings, an Olympia headquarters listing, Seattle-Tacoma regional pages, local phone numbers, map listings, reviews, or ratings. Those clues can help you build a shortlist, but they do not show how your invoice will be reviewed.

Search can also show early-stage programs, directory profiles, national rankings, freight providers, staffing and payroll-funding providers, software or receivables-administration companies, brokers, loan companies, and other business-service listings.

The provider type matters less than the quote. Start with one real customer and one real invoice, then compare what the quote shows: the advance, any reserve, fee, paperwork needed, payment instructions, funding timing, agreement terms, invoice choice, and who answers after setup.

| Provider type you may see | What it usually means | What to check before you choose |

|---|---|---|

| Local Tacoma office, Tacoma-based firm, Olympia headquarters listing, or Seattle-Tacoma regional provider | May show a Tacoma address, regional service page, Olympia map result, local phone number, reviews, or ratings. | A Tacoma office is not required. Check who reviews the customer, verifies the invoice, sends the advance, and answers after setup. |

| Very-early-stage or small-revenue factoring program | May focus on new companies or businesses below a stated monthly revenue level. | What customers and invoices qualify, what volume limits apply, and what setup, monthly, transaction, reserve, and agreement terms apply. |

| National ranking list, review site, or Washington factoring directory | May rank or list providers by fee, advance rate, industry fit, funding speed, software, or contract terms. | Use the list to collect names. Then compare your own customer, invoice, paperwork, written quote, and account support. |

| Company-name match that includes Tacoma but lists another state | A directory or search engine may match the company name to Tacoma even when the business is based elsewhere. | The actual company location, whether it serves Tacoma, who funds the invoice, and whether the listed terms apply to your business. |

| National independent direct factoring company serving Tacoma | Reviews the customer and invoice, factors approved invoices, sends the advance, receives the customer’s payment, and services the account without requiring a Tacoma office visit. | Whether one customer and one invoice are enough to start and whether the quote shows the advance, any reserve, fee, payment instructions, funding timing, agreement terms, invoice choice, and account support. |

| Freight or trucking factoring provider | Usually focuses on carriers, brokers, shippers, rate confirmations, PODs, bills of lading, fuel cards, fuel bundles, quick-pay wording, apps, load boards, or other carrier services. | Whether the broker or shipper can be approved, whether the load paperwork supports the invoice, and whether extra services affect fees, minimums, invoice choice, agreement terms, switching terms, or account support. |

| Staffing factoring company or payroll funding provider | May focus on staffing invoices, approved timesheets, weekly payroll, payroll processing, back-office services, tax filing, onboarding, or timekeeping. | Whether the service is invoice factoring, payroll processing, back-office administration, a payroll loan, or another product with different costs and responsibilities. |

| Software-connected, A/R administration, or credit-management provider | May connect funding to invoicing software or manage billing, payment tracking, credit review, or collections without buying the invoice. | Whether the provider buys approved invoices, what customer contact occurs, how fees are charged, and who answers after setup. |

| Broker, marketplace, consultation, or no-fee referral listing | May introduce you to one or more factoring companies instead of funding and servicing the account directly. | Who funds the invoice, whose agreement you sign, who services the account, and how the intermediary is paid. |

| Bank-backed, secured loan, credit line, equipment finance, asset-based, or purchase-order provider | May offer debt or another finance product instead of buying completed B2B invoices. | Whether the offer is invoice factoring or debt with different collateral, repayment, reporting, customer-notice, and exit terms. |

| Cold-storage facility, logistics company, financial consultant, or other search-result noise | May appear because a finance category, business-services category, industry term, or map result overlaps with the search. | Whether the listing actually buys approved unpaid B2B invoices, verifies the invoice, sends the advance, and services the account after setup. |

Orange Commercial Credit fits the national independent direct factoring category. It is headquartered in Olympia, Washington, and serves Tacoma businesses without requiring a Tacoma office visit. The review starts with one customer, one invoice, and the backup paperwork tied to the completed work.

One customer and one invoice are enough to see whether the written numbers work.

The details matter because the rate alone does not tell you what happens before funding or after your customer pays. A written quote should show the customer review, invoice review, advance, any reserve, fee, payment instructions, funding timing, agreement terms, invoice choice, and account support.

We're Orange Commercial Credit. We buy approved unpaid invoices for work you’ve already done. It’s called invoice factoring, and we’ve been doing it since 1979.

Through recessions, slow seasons, and the ups and downs of every business cycle, Orange Commercial Credit has kept clients funded so payroll, fuel, and repairs get paid even when your customers’ payments are still weeks away.

You send us your customer's invoice and once it's approved, we send you most of the money up front.

This up-front payment is called an advance. Depending on your industry, it can be as high as 98% of the invoice.

When your customer pays in full, on the next cycle you receive the remainder minus our factoring discount fee, which can range from 1.25% - 5%.

You choose which invoices to sell. Use it when you need it, skip it when you don’t.

We’ve been through decades of change, but one thing never changes: your bills don’t stop. That’s why your money shouldn’t wait.

Over the years we’ve worked with trucking companies, staffing firms, service providers and manufacturers just like you. Many have been with us five years or more.

They stay because the money’s there when they need it and because they value the service they receive.

They have one dedicated account executive who is backed by an experienced team ready to answer all their questions.

Most of our business comes from referrals. Our clients refer because they know their friends will get the same service they do.

A produce hauler told us what it feels like working with OCC:

“We love OCC! They have taken care of us since 2021. We have the pleasure of working with our account rep. She is such a big help. Always quick to respond to any questions or inquiries we may have. She is always available and I know that I can always count on her. She’s the best! Quick payment, great rates, excellent communication. A trusted company. Highly recommend.”

—Mariya, Owner-Operator, Produce Hauler

A trucking owner told us how she first came to OCC:

“I turned to my friend Mike for advice and he referred me to his factor… OCC. She reviewed my paperwork and explained step by step what I needed to do including outlining who to contact, what numbers to reference and what I needed to ask.”

—Alyssa, Owner, Long-Haul Trucking Company

With us, even if your customer pays on 30, 45, or 60-day terms, you’ll have the cash in your account; usually within 24 hours of invoice approval once you’re established as a client.

Factoring Invoices Since 1979

Trucking, staffing, and manufacturing companies in

Tacoma and across Washington use us when the wait gets too long.

One customer. One invoice. One call.

You get a person, not a menu:

1-800-231-3878

The only way this works is if your customer’s good for it. That’s why our credit check matters.

We’ve been doing this since 1979, and many of our credit team members have been here 10+ years. They know how to check credit right.

We focus on getting you paid faster on approved invoices.

It’s one thing to hear you’ll get paid...

Here’s what happens, step by step, from the time you send an invoice until the final payment clears.

In invoice factoring, the first thing we do is check your customer’s credit. We pull their payment history up front—even before you send us an invoice—because that’s how we decide if we can buy the invoice from you.

Once they're approved, you send an invoice, and our team then reviews the supporting paperwork that goes with it.

Once your invoice is approved and you're set up as a client, we notify your customer to send payment directly to us and confirm they’ve accepted the change.

It doesn’t change the work you did or the price on the invoice. It updates their Accounts Payable on where to send the payment.

The last step is the funding, the part you care about most.

That’s when the money hits your account.

On every funding you’ll see:

For some industries, we can advance up to 98% of the invoice within 24 hours. On a $10,000 trucking company invoice, that usually means $9,700 to $9,800 up front.

Depending on your company and your industry, we may hold back a small portion of the invoice as a reserve. Not all factoring agreements hold a reserve, but if yours does, it's a small amount set aside until your customer pays the invoice in full. It helps protect you against having to pay us out of pocket for any uncollectible portions of your invoices.

Typically, available reserve balances are refunded (minus our discount fee) on the next cycle following collections.

The discount fee depends on:

Whatever the case, we let you know the fee before you decide — no surprises.

That's how our factoring works.

Ready to see your numbers? You always see the advance, any reserve, and our fee before you decide. No surprises. Call and we’ll walk you through one invoice on the phone:

1-800-231-3878

The difference with us? We’re independent so we can set your terms the way you need them.

We don’t answer to outside investors. We’re privately held with no board calling the shots. We’re business owners too.

Your terms come from us, and no one else.

We know what it takes to meet payroll and keep the lights on. And we also know that every business is different. We don't drop numbers into a formula.

We base terms on what we see in your invoices and your customers, not on a one-size-fits-all chart.

One flatbed hauler said it best:

“It doesn’t matter if you bring $1 or a million, I guarantee you these people will treat you as a family member. We will always see these people as a great place for financial support and great customer care.”

—Rico, Flatbed Hauling

In the end, it comes down to trust. Who do you want to rely on when the bills can’t wait? With us, it starts simple: pick one customer, one invoice, and make one call.

You’re probably asking: So how would this work in my business?

The answer depends on the work you do.

We don’t fund most types of construction, third party medical receivables or consumer invoices. But we have funded companies across more than 50 industries.

We fund invoices for work that’s already done. The goods are already delivered, but your customer’s on terms.

The real issue is when the wait drags well beyond 30 or 45 days.

Let's walk through a few examples in trucking, staffing, and manufacturing, the industries where this matters the most.

Trucking advances can be as high as 98% of the invoice.

Orange Commercial Credit provides freight factoring for carriers that have delivered the load and invoiced a broker, shipper, or other B2B customer. We buy approved freight invoices so carriers can have money for fuel, repairs, payroll, and other bills before the broker or shipper pays. Freight factoring is also called trucking factoring.

Trucking companies are Orange Commercial Credit’s largest client group. For Tacoma, Pierce County, South Sound, and Washington carriers, our team reviews broker or shipper credit and the invoice packet: signed rate confirmation, bill of lading or POD, invoice, and paperwork for extra charges such as lumper fees or detention.

If you are comparing trucking factoring companies or freight factoring companies, a fast-approval claim, same-day headline, free credit check, fuel-card offer, fuel bundle, mobile app, load-board integration, or 24/7 funding headline does not show the full quote. Start with one broker or shipper, one delivered load, and the paperwork tied to that load.

The quote should show the advance, any reserve, fee, funding timing, agreement terms, invoice choice, customer payment instructions, and who answers after setup.

Tacoma and South Sound carriers may be hauling containers, breakbulk cargo, refrigerated freight, intermodal freight, drayage, warehouse loads, or regional deliveries through the Port of Tacoma Tideflats, I-5, SR 509, Port of Tacoma Road, Fife, and Pierce County. The question is whether the rate confirmation, bill of lading or POD, broker or customer approval, and funding timing match the freight invoice you need reviewed.

Ask whether the broker or shipper can be approved before you haul, what paperwork is needed after delivery, when the advance can be sent, whether a reserve applies, and how any available reserve releases after the customer pays.

Also ask whether the factoring offer includes recourse terms, non-recourse wording, monthly minimums, invoice-submission fees, ACH or wire fees, app or portal fees, fuel-card terms, fuel-bundle terms, or switching terms.

If a factoring offer includes a fuel card, fuel bundle, mobile app, load board, dispatch service, 24/7 funding, or another carrier tool, ask whether that extra service changes the fee, minimums, invoice choice, agreement terms, switching terms, or who answers after setup.

The written numbers are what let you compare the quote without guessing.

We work with all of them every day

and the story's always the same.

The load’s already hauled. The paperwork’s in. The only thing missing is the money in your account.

And the paperwork looks different depending on the job.

However you haul it, the wait is the same.

The load’s delivered, the paperwork’s in, and you’re still not paid.

Meanwhile, fuel, payroll, and repairs are due now. That’s when you sell us the invoice, and we send the advance after approval.

You’ve seen the ads: same-day funding, free credit checks, fuel cards, fuel bundles, mobile apps, and 24/7 payouts. Those features can matter, but the written quote still controls the numbers and conditions.

So the real question is:

Will the money actually

be there when you need it?

Once the broker or customer is approved, the invoice is verified, and the account is set up, we usually send most of the money within 24 hours.

And what about brokers?

You may not know how one has been paying before you book the load.

That’s what our credit team reviews every day. We check broker and shipper credit before you haul, so you can see whether the customer can be approved before you count on that invoice for funding.

We’ve been doing this since 1979. Many on our credit team have been here more than ten years.

That experience matters when the broker, invoice, and paperwork need review and you need an answer tied to the load.

Friday payroll comes due. Fuel card drafts this week. The truck note hits this month.

And the shop won’t release a truck until the repair’s paid. Plus, you need tires and have insurance renewals.

Carry a balance on your card, and the interest adds up.

Fuel bills spike, and drafts hit your account whether or not a broker’s check has cleared.

None of those bills wait.

You need to get paid.

If your trucks are hauling through Tacoma, the day can turn on the Port of Tacoma Tideflats, I-5, SR 509, Port of Tacoma Road, 34th Avenue E, East D Street, Norpoint Way NE, the Blair Waterway, Schuster Parkway, the Puyallup River bridge, terminal gates, rail timing, and customer delivery windows.

At the Tideflats, container terminals, breakbulk cargo, grain exports, warehouse space, transload yards, heavy-haul routes, and rail-served docks can put drayage trucks, flatbeds, reefers, and local delivery runs into the same gate schedule.

On SR 509, overweight container routes can require the right corridor, the right permit, the right truck setup, and the right timing before the load clears the port side.

Around I-5 and Port of Tacoma Road in Fife, ramp work, one-way route changes, night lane closures, and off-ramp queues can push a pickup window back before the truck reaches the terminal.

When one terminal gate, RFID check, rail handoff, dock slot, heavy-haul route, I-5 queue, or Blair Waterway vessel delay runs late, the delivery window gets tighter and the next load starts late.

If the delivery window closes, the load waits.

You still have fuel to buy.

Payroll is Friday. Your customer may still be paying on 30, 60, or 75 day terms.

A fleet owner put it this way:

“Amazing people working at this company! Always a phone call away always eager to help and always getting the issues solved. Great % rates and overall great people starting from managers to accountants and assistants. Been working with them for over 4.5 years with no problems or complications what so ever.”

—Vitaliy, Interstate Freight Carrier

An intermodal freight fleet owner told us what OCC meant for his business:

“Orange Commercial Credit (OCC) was instrumental in our growth from the very beginning. They not only understand the trucking industry but also specialize in the intermodal and drayage business. The funding is quick, the relationships are deep, the rates are fantastic, and the trust earned is invaluable. I have been able to personally recommend OCC to many of our Clients over the past years and have always heard great feedback in return. Thank you OCC for your commitment and friendship. Clients like me really do appreciate it!”

—Michael S., President, Intermodal, Client since 2013

A long-haul carrier told us why the credit check matters:

“OCC is an exceptional factoring company! Not only do they help us with our invoices, but also advise us on broker credibility, ensuring that we are getting paid for our work. I would like to express my sincere appreciation to my AE for her prompt responses to my inquiries. It makes a real difference.”

—Tom A., Long-Haul Trucking

Tom’s quote shows what a fleet counts on with credit checks. But when it’s just you and your truck, it’s fuel, repairs, insurance, and the bills waiting at home. All on you.

Fuel card drafts hit every week. The truck note’s coming due. Add shop repairs and home bills. Waiting 30–45 days for a broker to pay just doesn’t cut it.

That’s why we usually send the money within 24 hours; so it’s there before the next bill hits.

Here’s how another owner-operator put it after using OCC for years:

“I'm a small carrier owner operator.

I've been using Orange Commercial Credit for about 4 years now and I couldn't be more happier with the service provided by OCC.

OCC is very fair with their rate and they pay out very quickly (next day).

Their staff is great, very professional and nice.

I recommend OCC for all carriers who need a factoring company.”

—Ezechiel, Owner-Operator, OCC client since their first load

Ezechiel’s an owner-operator, and the bills don’t wait any less when you’re hauling hot shot loads.

Hot shot runs are smaller, but the bills still stack up just as fast.

Whether you're in an F-350, a Ram, or a Duramax with a gooseneck or bumper-pull, one stretch of repair and fuel bills can drain your cash fast.

You could really use that new Big Tex tandem dual wheel, but trailer payments stack up fast.

And if a broker’s been paying slow, you hear it from us before you waste the trip, not later.

A hot shot driver explained why she sticks with OCC:

“Orange Commercial Credit is an excellent company to work with. They offer exactly what we need to run our trucking company, we always know what brokers are safe to work with due to Orange’s credit check feature. Staff is always friendly and helpful. I have never had a bad experience with our assigned Account Executive or any other staff member for that matter, the whole team is great!”

—Crystal, Hot Shot Trucking

You’ve done the work. You shouldn’t be waiting a month to see the money.

Most clients start with just one customer, one invoice, and one call to us. Even if you just have a question, call us. We'd be happy to talk with you.

If you’re running loads in or out of Tacoma or anywhere in Washington, we can walk through one invoice on the phone:

1-800-231-3878

We’ve been checking broker and shipper credit since 1979.

Staffing advances can be as high as 90% of the invoice.

Orange Commercial Credit provides payroll funding for staffing companies through invoice factoring. We buy approved unpaid B2B invoices so staffing agencies can have money for payroll before customers pay.

If you are comparing staffing factoring companies or payroll funding companies, start with one customer, one invoice, approved timesheets, the service agreement or customer approval, and the written quote.

Tacoma and Pierce County staffing firms may be filling Tideflats warehouse shifts, Fife logistics crews, Frederickson manufacturing roles, Puyallup light-industrial work, healthcare positions, skilled trades, or JBLM-area assignments while customers remain on 30, 60, or 75-day terms. The review still comes back to the customer, invoice, approved timesheets, and written numbers.

Once the customer is approved, the invoice and timesheets are verified, and the account is set up, we usually send most of the money within 24 hours.

If you run a staffing agency, payroll means two things: the recruiters in your office and the workers already out on site.

Timesheets get signed, checks go out every Friday, and customers may not pay for 30, 60, or more days.

The hours are already worked. Payroll’s due. The money isn’t in yet.

However you staff it, the work is done and you’re still waiting to get paid.

And it’s never just wages. You've got:

Ask whether the customer can be approved, whether the approved timesheets support the invoice, when the advance can be sent, whether a reserve applies, and how any available reserve releases after the customer pays.

Also ask whether the offer includes recourse terms, non-recourse wording, monthly minimums, invoice-submission fees, ACH or wire fees, portal fees, payroll-processing charges, back-office charges, or switching terms.

If a payroll funding offer includes back-office services, payroll processing, tax filing, timekeeping software, onboarding tools, or recruiting services, ask whether that extra service changes the fee, minimums, invoice choice, agreement terms, switching terms, or who answers after setup.

The written numbers are what let you compare the quote without guessing.

If your staffing orders run through Tacoma, the week can turn on Tideflats warehouse shifts, Frederickson industrial roles, Fife logistics crews, Puyallup light-industrial work, Tacoma hospital coverage, skilled trades, forklift operators, inventory clerks, and worker start times.

Around I-5, Port of Tacoma Road, South Pine Street, Marine View Drive, Frederickson, Fife, Puyallup, the Port of Tacoma corridor, and the JBLM side, a staffing order can require drug screens, background checks, credentials, VMS entries, reliable transportation, or same-week availability before the worker clocks in.

Warehouse, healthcare, logistics, aviation, manufacturing, IT, engineering, skilled-trade, and day-labor roles can all pull from the same Pierce County worker list in the same week.

When one worker callout comes in, one credential waits, one VMS entry is blocked, one day-one orientation is missed, or one I-5 delay slows the morning commute, the agency still has to fill the shift and run payroll.

If a shift is not filled, the hours are not billed.

You still have rent, insurance, payroll taxes, workers’ comp, and recruiter payroll to pay.

Payroll is Friday. Your customer may still be paying on 30, 60, or 75 day terms.

Without funding, some owners try to stretch their own payables or pay bills with credit cards. Others dip into personal savings, just trying to bridge the weeks until customers finally send payment.

A staffing owner explained how OCC let him take on more customers:

“I can always count on them. Orange Commercial has helped me take on clients I normally could not afford to take. The setup process with them was easy. They let you choose which clients you want to factor. Pricing is reasonable for the industry. Customer service is great and I can always count on them to send me funds when I need it.”

—George, Owner and Client Since 2016, Staffing Company

A staffing owner told us how OCC changed his cash flow:

“As a staffing company owner, I heavily rely on cash flow to keep my operations running smoothly and meet payroll, OCC's factoring process is incredibly streamlined and hassle-free. Their newly implemented online platform is user-friendly, making it easy for me to submit and track invoices. This new system allows me to receive funds quickly and efficiently, greatly improving my cash flow management. I highly recommend them.”

—Joe, Owner, Staffing Company,(Client since 2018)

And that’s how factoring works in staffing. A lot of owners call it payroll funding. Payroll runs every week, along with taxes, insurance, and benefits. With Orange Commercial Credit, the funds are there so checks go out on time.

You’ve made payroll. You shouldn’t be carrying it for weeks while customers take their time.

Bring one customer, one invoice, and approved timesheets. We’ll review the customer and paperwork, then show the advance, fee, any reserve, and timing before you decide.

Most agencies start with just one customer, one invoice, and one call to us.

If you have one question, call with one customer name and one invoice in mind:

Staffing advances can be as high as 90% after customer approval and invoice verification.

You see the advance, any reserve, fee, and timing before you decide.

Manufacturing advances can be as high as 90% of the invoice.

Orange Commercial Credit factors approved unpaid B2B invoices for manufacturers that have completed the work, delivered the goods, and invoiced a customer on terms.

For Tacoma, Pierce County, South Sound, and Washington manufacturers, the review can include the customer, invoice, purchase order, bill of lading, packing list, delivery proof, work ticket, or signed QC paperwork tied to the completed order.

Tacoma-area manufacturers may be buying raw materials, paying suppliers, scheduling shop work, repairing machinery, or moving finished goods through the Tideflats, Frederickson, Fife, Puyallup, and the Port of Tacoma corridor while customers remain on 30, 60, or 75-day terms.

Once the customer is approved, the invoice is verified, and the account is set up, we usually send most of the money within 24 hours.

Staffing firms feel it every Friday. Manufacturers do too, just with different bills.

Yes. Purchase-order financing, asset-based lending, equipment financing, inventory finance, supply-chain finance, and invoice factoring can all appear in Tacoma manufacturing search results. The question is what the money is tied to: a purchase order, finished goods, a verified invoice, equipment, inventory, receivables, or another credit facility.

Purchase-order financing may be reviewed before finished goods are delivered. Asset-based lending or equipment financing may depend on collateral, reporting, repayment, and other credit terms. Invoice factoring starts after the work is complete, the customer can be reviewed, and the invoice backup supports the bill.

Before you decide, ask which product is being quoted, what paperwork is needed, what advance is offered, whether a reserve applies, what fee applies, where the customer sends payment, and when any available reserve can release.

If your manufacturing work runs through Tacoma, the day can turn on the Tideflats, Frederickson Manufacturing/Industrial Center, Canyon Road East, SR 509, Port of Tacoma breakbulk terminals, the Foss Waterway side, 70th Avenue East, FRED310, raw materials, machines, inspections, and customer delivery dates.

Around Tacoma’s maritime, aerospace, plastics, polymer, machining, life-sciences equipment, metal fabrication, warehouse, and heavy industrial work, one order can require port cargo, raw materials, CNC time, molded parts, crane access, QC records, or supplier paperwork before the finished work can turn into a paid invoice.

A shop floor can wait on Canyon Road freight delays, SR 509 heavy-haul routing, breakbulk cargo timing, utility capacity, stormwater requirements, environmental review, machine time, or trained labor before the next production step starts.

When one material lot is late, one machine is down, one inspection waits, one supplier delivery misses the dock time, or one port-side delay holds raw materials, the next production step waits too.

If materials are late, the line waits.

Power, rent, supplier invoices, and payroll keep running.

Payroll is Friday. Your customer may still be paying on 30, 60, or 75-day terms.

Suppliers want to be paid in 15 to 30 days. Customers may take 45 to 60 days or longer. The customer may not send payment until every piece of paperwork lines up:

By the time you deliver and gather it all, you may have cut the checks weeks ago. You are still waiting for the customer’s payment.

And this is where factoring

helps in manufacturing.

You send the invoice and backup paperwork. We review the customer and invoice. Once the customer is approved, the invoice is verified, and the account is set up, we usually send most of the money within 24 hours.

A pallet manufacturer told us how OCC became part of their growth:

“I’ve been working with OCC for over 9 years now and they’re like a partner for me.

I could not have grown my business this quickly without them!

My account executive is great.

I get credit checks done same day on new business and have never had a complaint from any customer.”

—E.H., President, Pallet Manufacturer

A machine shop owner found that factoring with OCC was "very easy to work with":

“Finding out about OCC has helped keep my business operating with the cash flow I am now receiving. Within a day the money is in my account. During the whole process, OCC was very easy to work with. They made sure I was completely confident and work with me step by step, and the staff is very patient. I would recommend them to any business. Once you start with OCC, you will also be recommending them.”

—Val, Owner and Client Since 2017, Machine Shop

Whether it’s pallets, plastics, machining or food processing, if you’ve already delivered and sent the invoice, you don't need to be waiting 45 to 60 days for payment.

Bring one completed B2B invoice. We’ll review the customer, invoice, and backup, then show the advance, fee, any reserve, and timing before you decide.

Pull one completed B2B invoice from one customer. Call, and we’ll show the advance, fee, any reserve, and timing before you decide.

Manufacturers in Tacoma and across Washington use us when customer terms run long.

Here's another benefit to factoring

you may not be aware of:

If you’re a pallet manufacturer sending a quote, a distributor supplying parts, or a service firm chasing contracts, you’ve heard it:

“Can you give us Net-30?”

Sometimes Net-45. Buyers ask for it every day. And if you can’t offer it, they move on. With factoring in place, you can say yes without tying up your own cash.

Longer terms can:

What matters most is whether your customer is likely to pay, and whether the invoice is clear, verified, and tied to completed B2B work.

Tax liens, pledged invoices, or another lender’s claim on receivables can slow the review, but we will tell you what paperwork or release is needed.

Start with one customer and one invoice. We will review what you have and tell you whether we can continue the review or what is still missing.

Call us and we will go over one of your customer’s invoices together.

Orange Commercial Credit’s portal shows invoice and payment status, paperwork, and credit information tied to your account, so you can see where each invoice stands.

You do not have to wonder

whether a payment posted to the right invoice.

Your paperwork is reviewed by an experienced team. Many have been here ten years or more and know the customers and documents tied to your account.

No. You get a dedicated account executive who knows your business, your customers, and the paperwork already reviewed for your account.

When you call, you can talk to the same person instead of explaining the same invoice again. Your account executive is backed by an experienced team when another review is needed.

A logistics company shared what its experience with OCC has been like:

“We have been with OCC for the last 3 years and have had a great relationship. OCC has been a very important part in our business. With their quick credit information on new prospect customers is the key to eliminate any accounting issues.

We submit our invoices through their scanning program and are funded same day with no problems.

We have not had any problems or complaints from our customers as they are very kind and professional to them.

I highly recommend OCC if you are looking for a reliable and honest Factoring Company.”

—Mary, Operations/Accounting, Logistics Company

No. Invoice factoring is not a traditional loan. You sell an invoice for work already completed, so there is no new monthly loan payment tied to that invoice sale.

It is money your customer already owes. Factoring lets you receive most of that money sooner after the customer is approved, the invoice is verified, and your account is set up.

A factoring company buys approved unpaid B2B invoices so a business can receive an advance before its customer pays on terms.

The review starts with the customer, invoice, and backup paperwork tied to the completed work. Before you decide, the written quote should show the advance, any reserve, fee, payment instructions, funding timing, agreement terms, invoice choice, and who answers after setup.

The process starts with completed B2B work, an invoice, and the backup paperwork tied to that work.

Compare the advance rate, factoring fee, any reserve, customer approval process, paperwork needed, payment instructions, funding timing, agreement terms, invoice choice, minimums, and who answers after setup.

A ranking, map listing, local address, fast-funding headline, low-fee claim, fuel-card offer, or high-advance claim does not show the full quote. Start with one real customer and one real invoice, then compare the written numbers.

You can start with one customer and one invoice. It also helps to know your industry, the invoice amount, typical monthly invoice volume, the customer’s payment terms, and what paperwork supports the completed work.

Monthly volume and payment terms can help you compare quotes, but you do not need everything ready before the first call.

Yes. Orange Commercial Credit is a national independent direct factoring company headquartered in Olympia, Washington, and serving Tacoma, Pierce County, South Sound, and Washington businesses without requiring a Tacoma office visit.

We review the customer, invoice, and backup paperwork, send the advance after approval and verification, receive the customer’s payment, and service the account after setup.

Factoring fee range: 1.25% to 5% (varies by deal).

The discount fee is a percentage of the invoice. How much depends on your industry, how fast your customer pays, your customer’s credit, and the dollar amount of invoices you sell us.

You always see the cost up front before you decide.

Applicable ACH or wire fees may be deducted as described in the written program.

Money-transfer fees may include a $2 ACH send fee or a $12 wire send fee, depending on the program. A wire is optional. Ask your bank whether it also charges a wire receiving fee.

Use this list to see the full cost and agreement terms before you decide.

If you only ask three, start here:

Full checklist:

1) Advance rate:

This is what you receive up front. A lower advance can mean you are waiting on more of your own money until your customer pays.

2) Factoring fee:

Ask what the fee covers: per 10 days, per 30 days, daily, or flat. If it is tiered, ask for the full tier schedule in writing.

3) Recourse period (how long the invoice can stay open):

Ask what happens if your customer still has not paid by then.

4) Recourse or non-recourse (who takes the named loss risk if the customer does not pay):

Ask what “non-recourse” covers and what it does not cover.

5) Customer credit concentration limits (how much the provider will fund for one customer):

Ask what the limit is if one customer is a large share of your billing.

6) Reserve:

This is what may be held back. Ask when any available reserve releases and what deductions may apply.

7) Transfer fees:

Ask about ACH send fees, wire send fees, and any receiving fee charged by your bank.

8) Minimums or commitment fees:

Ask whether you pay a fee when you do not factor enough in a slow month.

9) Other fees:

Ask for a full list of setup, portal, monthly, invoice, due-diligence, termination, and buyout fees.

10) Contract term:

Ask how long you are agreeing to, how the agreement renews, and what notice date applies.

11) What notice do you need to stop factoring?

Ask what proper notice means if you move to another factor or no longer need factoring.

The quote should be in writing so you can compare the advance, fee, reserve, timing, and agreement terms.

Factoring companies may use several agreement labels. The label is only a starting point. The written agreement controls what happens if a customer pays late, disputes the invoice, short pays, or does not pay.

Ask what event is covered, what happens after a dispute or short pay, whether an unpaid invoice must be replaced or repurchased, what minimums apply, which invoices you may choose, and what happens when the agreement ends.

Orange Commercial Credit offers a 90-day factoring agreement, no setup fee, no minimum number of invoices, and invoice choice. The written proposal shows how those terms apply to your customer and invoice.

No. Orange Commercial Credit lets you choose which invoices to factor. One customer and one invoice are enough to start the review.

The starting point is completed B2B work, an invoice, a customer that can be approved, and backup paperwork tied to the work.

Orange Commercial Credit does not fund most construction claims, third-party medical receivables, or consumer invoices.

No. Those are our largest groups, but we also factor approved invoices for logistics, warehouse, industrial service, commercial service, oilfield-related service, janitorial, security, road-flagging, commercial cleaning, autobody repair, and other B2B companies.

No. We work with companies in Tacoma, across Washington, and throughout the United States. One customer, one completed B2B invoice, and the backup tied to the work are enough to start the review.

No. Orange Commercial Credit is headquartered in Olympia, Washington, and serves Tacoma businesses without requiring a Tacoma office visit.

A factoring company does not need a Tacoma office to factor approved invoices for a Tacoma business.

Customer approval is based on commercial credit review, payment-history information, invoice verification, and the backup paperwork tied to completed work. It is not based on the factoring company’s address.

Before you decide, we show the advance, any reserve, fee, payment instructions, and funding timing in writing.

Compare the written quote first. It should show who reviews the customer, who checks the invoice, what advance is offered, whether a reserve applies, what fee applies, and who answers after setup.

Search results can mix target-city pages, Olympia headquarters listings, Seattle-Tacoma regional providers, map listings, reviews, directories, national rankings, brokers, lenders, and national factoring companies serving the South Sound.

Use those results to collect names. Then compare the customer review, invoice review, advance, any reserve, fee, payment instructions, timing, agreement terms, invoice choice, and account support.

Check the actual company address, the company that will fund the invoice, whose agreement you will sign, and who will service the account. A name or directory heading does not prove the provider has a Tacoma office or directly funds Tacoma invoices.

Ask whether the product is invoice factoring for completed B2B work, what minimum invoice or monthly volume applies, whether the customer must be approved, what paperwork is required, what fee applies, and who funds and services the account.

Ask for the complete written quote. It should show whether the rate is flat, daily, or tied to a time period; the advance and reserve; startup and transfer fees; monthly minimums; renewal terms; notice needed to leave; and who answers after setup.

Ask whether the claim refers to application review, account setup, customer approval, invoice verification, or the actual advance. The written conditions should name customer approval, invoice verification, signed agreement terms, account setup, cutoff time, and bank timing.

A broker, directory, ranking, or referral listing can help you collect names. Ask who actually funds the invoice, whose agreement you sign, who services the account, and how the intermediary is paid.

Orange Commercial Credit is a direct factoring company. We review the customer and invoice, send the advance after approval, receive the customer’s payment, and service the account.

Not always. Those services may manage receivables, send statements, review credit, or collect balances without buying the invoice. Ask whether the provider purchases approved invoices or only performs administrative or collection work.

No. Loans and credit lines are debt products. Equipment finance is tied to equipment. Purchase-order finance may be reviewed before finished goods are delivered. Invoice factoring starts after completed B2B work has produced an invoice that can be verified.

Search can mix a finance category, local business-services category, address, or industry term with the factoring query. Check whether the listing actually buys approved unpaid B2B invoices, verifies the invoice, sends the advance, and services the account after setup.

Yes. Orange Commercial Credit factors approved freight invoices for Tacoma, Pierce County, South Sound, and Washington carriers after the broker or shipper is approved and the invoice packet supports the completed load.

The packet may include the invoice, signed rate confirmation, bill of lading or POD, and accessorial backup when billed.

Once the broker or shipper is approved, the invoice is verified, and the account is set up, we usually send most of the money within 24 hours.

Yes. Ask whether an extra carrier service changes the factoring fee, minimums, invoice choice, agreement terms, switching terms, or account support. The broker or shipper still needs review, and the delivered-load paperwork still needs to support the invoice.

Compare the advance, fee, any reserve, broker or shipper approval, rate confirmation and bill of lading or POD review, recourse or non-recourse wording, monthly minimums, invoice choice, transfer fees, switching terms, and who answers after setup.

In many searches, yes. Freight factoring, trucking factoring, transportation factoring, and freight bill factoring usually describe a carrier selling an approved freight invoice instead of waiting for the broker or shipper to pay on terms.

Some providers require monthly volume or invoices from certain customers. Orange Commercial Credit lets you choose which invoices to factor and has no minimum number of invoices required.

Yes, through invoice factoring. We factor approved unpaid B2B staffing invoices so a Tacoma agency can receive an advance before its customer pays on terms.

The review starts with the customer, invoice, approved timesheets, service agreement, and other backup needed to verify completed work.

In many staffing searches, yes. Staffing factoring, staffing invoice factoring, staffing agency factoring, and payroll funding often describe selling approved B2B invoices before the customer pays.

Payroll processing, tax filing, timekeeping, recruiting, and back-office administration are separate services. Compare them separately from the factoring quote.

Compare the advance, fee, any reserve, customer approval, approved-timesheet review, payment instructions, weekly timing, monthly minimums, invoice choice, agreement terms, back-office charges, and who answers after setup.

Some do. Orange Commercial Credit has no minimum number of invoices required, and you choose which approved invoices to factor.

Invoice factoring addresses the wait between an approved staffing invoice and the customer’s payment. Back-office services may include payroll processing, tax filing, timekeeping, onboarding, or recruiting.

Compare them separately. Ask what each service costs, what work it performs, whether it changes the factoring fee or agreement terms, and who answers after setup.

Yes. We factor approved unpaid B2B invoices for Tacoma and Washington manufacturers after the customer is approved, the invoice is verified, and the backup supports the completed order.

Backup may include a purchase order, bill of lading, packing list, delivery proof, work ticket, signed QC paperwork, or other documents tied to the completed work.

Yes. Purchase-order financing may be reviewed before goods are delivered. Asset-based lending, equipment finance, inventory finance, and credit lines may depend on collateral, reporting, and repayment terms. Invoice factoring begins after completed B2B work produces an invoice that can be verified.

In an invoice factoring arrangement, the customer sends payment according to the factoring company’s written instructions.

That does not automatically mean the factoring company is responsible for every dispute or collection task. Ask who verifies the invoice, who answers payment questions, who follows up if payment is late, and who works through a dispute or short pay.

At Orange Commercial Credit, as the last step before funding, we contact your customer to verify the invoice and confirm where your customer sends payment.

No. They keep the same price and terms from you.

As the last step before funding, we contact your customer to verify the invoice and confirm where your customer sends payment.

If your customer has a question or something is missing, you work it out with them directly. Once the missing item is fixed, we can finish the review and send the advance if the invoice is approved.

Most of our team has been here ten years or more. They know the paperwork and can answer questions tied to the invoice.

Yes. Receivables factoring, accounts receivable factoring, A/R financing, A/R funding, and invoice factoring often describe the same basic arrangement. You complete the work and invoice your customer. We review the customer and verify the invoice. After approval and account setup, we send the advance. Your customer pays according to the written instructions. When payment posts to our bank, any available reserve releases under the agreement terms.

But it’s not on you.

We get it.

There’s no setup fee. You can review the proposal before you decide.

Most times, you’ll have an answer

by the next business day.

If the proposal looks right to you, we’ll set up an agreement. It’s a 90-day factoring agreement with no minimum number of invoices required.

It's there when you need it. You’re just giving yourself room to try it and see how it feels.

The agreement lays out the basics:

Once an invoice is approved, the advance is usually sent within 24 hours.

A staffing owner put it this way:

“I can always count on them to send me funds when I need it.”

—George, Owner and Client Since 2016, Staffing Company, KY

No minimums, no quotas. You decide when to use it.

You also get a dedicated account executive who knows your business and picks up when you call, answering your questions on the spot.

And you can log in any time day or night to check on balances and invoices.

If it makes sense, great. If not, you’ll still leave knowing more than you did before.

And for the owners who don't put it off,

here’s what it looks like.

An intermodal owner told us what makes it work:

“We submit our invoices almost daily using their scanning program, and know that when we submit before the deadline we get same day funding.”

—Mike, President Intermodal Transportation & Warehousing Company, and Client Since 2006

Once the invoice is approved and the account is set up, we usually send the advance within 24 hours. Payroll runs, fuel gets bought, and shop bills get paid.

That’s why we tell owners:

if the numbers make sense, you can decide from there.

Most owners start with just one invoice. That is enough to see how the numbers work.

In the end it always comes

back to the same thing:

one customer,

one invoice,

one call.

Call with one customer name and one invoice in mind. We’ll tell you what paperwork we need, review whether the customer can be approved, and show the advance, fee, any reserve, and timing before you decide.

For a real conversation:

1-800-231-3878

Independent and privately held

since 1979.

No setup fee, no minimums, and you talk to a person who knows your account.

🌙

After hours? No problem.

After hours, or if you’d rather not call, fill out this form and we’ll call you back.

Related Washington factoring company pages